Buying a home in places like Hawaii and California can take up to 70% or more of local per capita income.

Before the rise of remote work and the surge in demand for larger living spaces during the COVID-19 pandemic, the U.S. housing market was more balanced. Early in 2020, with a 30-year fixed mortgage rate of around 3.6%, the typical homeowner spent about 22% of their monthly per capita income on mortgage payments. In contrast, renters paid about 33% of their income on rent, which often made buying a home more attractive.

However, this advantage for homeowners has reversed. By May 2024, renters’ share of income for housing increased to 34.4%, while homeowners’ share surged to nearly 40%. This shift is due to rising home prices and mortgage rates that briefly peaked at nearly 7.8% in October 2023 before settling between 6.8% and 7% in recent weeks.

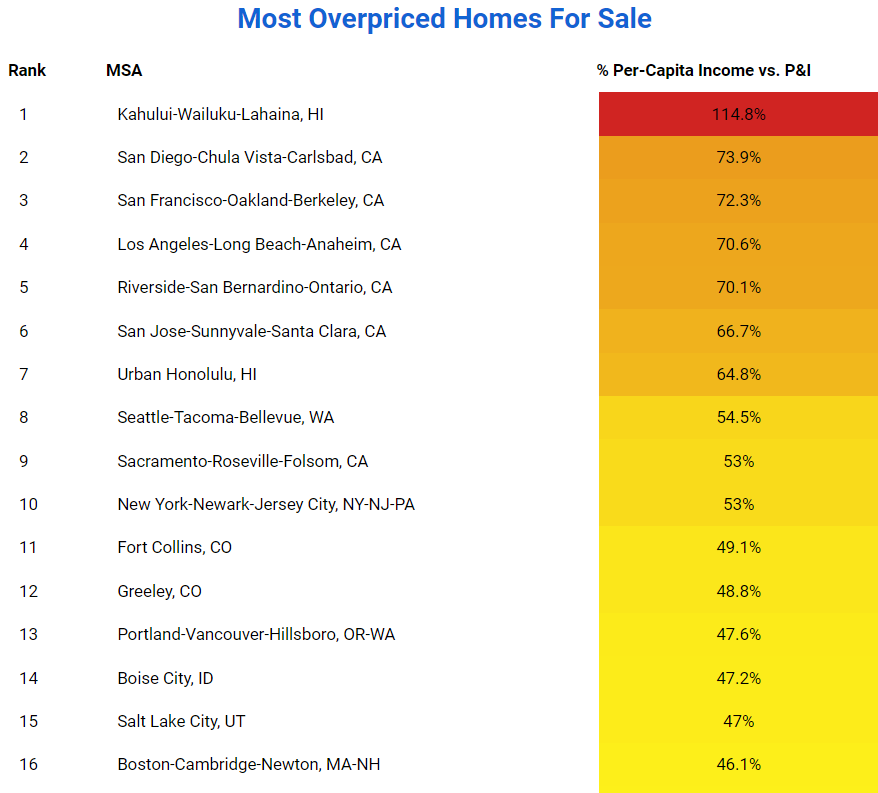

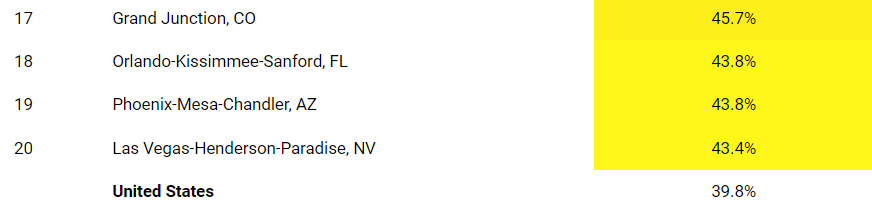

These national figures mask significant variations across different markets. In some areas, homeowners may spend up to two-thirds of their income on mortgage payments alone, and renters might spend more than half. As a result, many metropolitan areas appear overvalued relative to local earnings. For this analysis, markets where housing costs exceed the national median payment-to-income ratio of 39.8% for homeowners or 34.4% for renters are considered overvalued. Data for these rankings is sourced from the U.S. News Housing Market Index, which provides a data-driven overview of the housing market.

Here are some of the most overvalued metropolitan statistical areas (MSAs) based on payment-to-income ratios, all exceeding 70%:

– Kahului-Wailuku-Lahaina, Hawaii – 114.8%

– San Diego-Carlsbad, California – 73.9%

– San Francisco-Oakland-Hayward, California – 72.3%

– Los Angeles-Long Beach-Anaheim, California – 70.6%

– Riverside-San Bernardino-Ontario, California – 70.1%

In Hawaii, particularly in the Kahului-Wailuku-Lahaina MSA (which includes Maui, Lanai, and most of Molokai) and the urban Honolulu MSA (Oahu), high housing costs are a long-standing issue. Factors include a chronic housing shortage, a high influx of second-home buyers and wealthy transplants, and geographic challenges. The August 2023 wildfires in Maui exacerbated the problem, raising concerns that rebuilt homes may mainly serve affluent buyers rather than local residents, contributing to the displacement of native Hawaiians and locals.

In California, a persistent shortage of housing supply relative to job growth has led to high housing costs. Residents often cope by sharing housing, commuting long distances to more affordable areas, or relocating out of state. Some overvalued markets in states like Washington, New York, and Colorado also show payment-to-income ratios above 50%. With the U.S. median payment ratio at 39.8%, if mortgage rates remain high, some home prices may need to adjust to become more affordable for average buyers.

The Most Overvalued MSA to Buy a Home

While there are numerous reasons the housing market in the Kahului-Wailuku-Lahaina MSA housing market is overvalued compared with local per capita income, the primary one is because housing on Maui, known as “The Valley Isle,” is both popular and limited. Still, given recent surges in median sales prices, months of inventory have also climbed to levels indicating more of a buyer’s market.

Though the national median sales price of a home rose 4.8% year-over-year through May to nearly $439,000, in the Kahului MSA it surged 22.1% to approach $1.2 million – almost three times higher. In June the median sales price of a home in Kahului MSA jumped nearly another $100,000 to almost $1.3 million, versus about $443,000 nationally. Still, these rising prices are also leading to more inventory for sale, with the housing supply timeline in Kahului rising to 6.8 months in May versus just 2.4 months nationally (and in June rising further to 8.8 months versus 2.6 months nationally). If four to six months is considered a balanced market, Kahului is rapidly becoming a buyer’s market, and asking prices could soften over the next few months.

To address the housing shortage in the state, Hawaii Gov. Josh Green, who was sworn into office in December 2022, has made providing more dwelling units a cornerstone of his administration. In May 2024, his office hosted a signing ceremony for a series of bills focused on unlocking more housing throughout the state.

These bills include encouraging more accessory dwelling units (ADUs) on all lots currently zoned for residential development, prohibiting private covenants (such as HOA covenants, conditions and restrictions) from restricting ADUs, expediting the approval process for more affordable housing units by making it easier to seek exemptions from certain state laws and rules, allowing for the adaptive reuse of underutilized commercial spaces and office buildings for housing, issuing bonds to finance housing-related regional infrastructure projects (particularly in areas close to public transit) and funding a new task force to continue guiding long-range plans.

Another series of bills signed in May are intended to “streamline processes, enhance management practices and increase accessibility to clean energy programs for condominium communities” throughout the state, thereby encouraging more new condominium production. Although more than 60,000 new housing units are in the pipeline (including 13,000 affordable housing units proposed by 2026), it will take some time for these homes to be completed, sold or rented.

Overvalued Homes for Rent

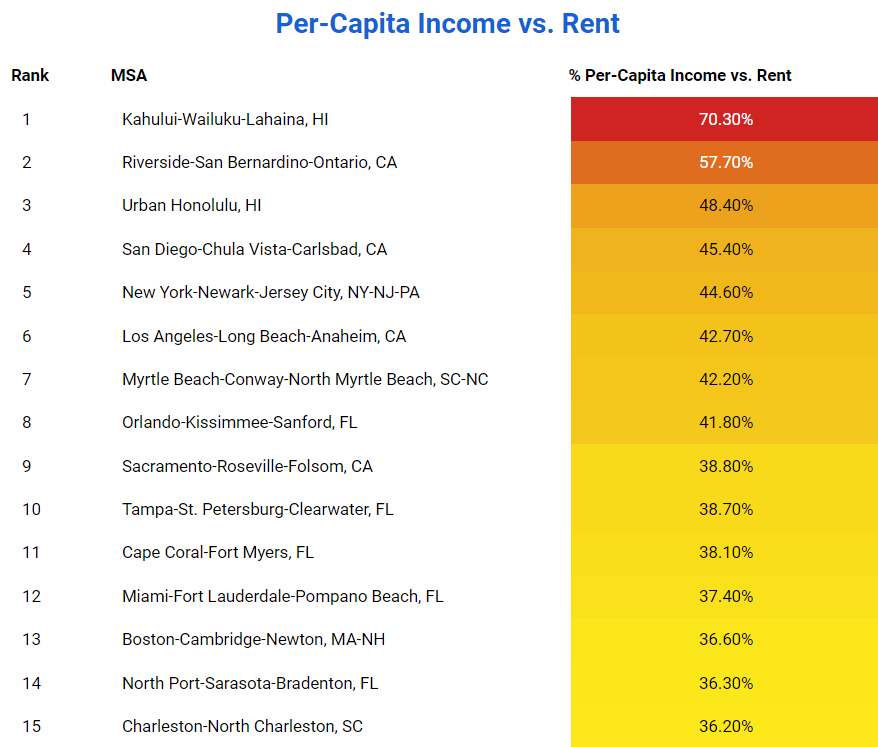

If you’re waiting for mortgage rates to subside further to decide on the right time to jump into the housing market, you should find out if you live in an MSA with an rent-to-income ratio far above the national median of 34.4%, which could make the leap to homeownership easier. In terms of overvalued rental housing markets, this list is led again by two markets in Hawaii as well as in California’s Riverside-San Bernardino-Ontario (which includes the “Inland Empire” east of Los Angeles), San Diego and New York City. In these markets, rent-to-per-capita-income ratios range from nearly 45% to over 70%:

Kahului – 70.3%

Riverside-San Bernardino-Ontario, California – 57.7%

Urban Honolulu – 48.4%

San Diego-Chula Vista-Carlsbad – 45.4%

New York-Newark-New Jersey, NY-NJ-PA – 44.6%

The Most Overvalued MSA to Rent a Home

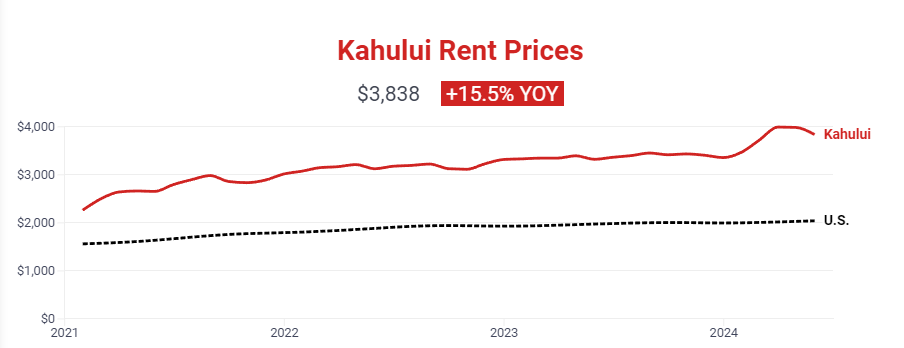

Besides being ranked as the most overvalued market to buy a home, the Kahului MSA also ranks at the most overvalued region to rent a home because its rental rates have risen faster than local incomes.

As of May 2024, the national median asking rent increased 3.4% year-over-year to $2,042 per month. By comparison, rents in the Kahului MSA jumped 15.5% year-over-year to $3,838 per month, or 187% higher.

In addition to the May housing bills signed into law, during that month Gov. Green also approved another bill giving the state’s counties more authority in regulating short-term rentals in their communities. The rise of short-term rentals in the state (including illegal units being operated where they are not authorized) has been partially blamed for the lack of affordable housing options targeted toward long-term residents.

Owning vs. Renting

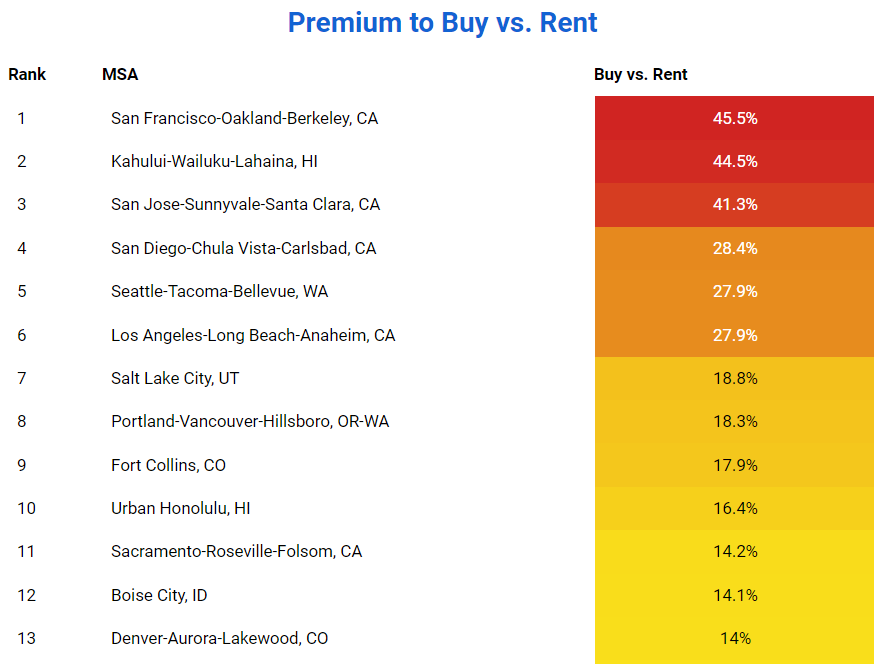

If you’re looking to determine the best time to enter the housing market, another metric to study is the difference between the cost of owning versus renting in a particular MSA. Notably, whereas the difference between these ratios for the entire country is just 5.4%, for other MSAs it can reach well over 40%. In these markets, the ability to buy a home is open to mostly the wealthy or existing homeowners with sufficient equity to carry over a large down payment to their next home.

The following six MSAs (with a tie for fifth place) are those in which the cost to own is nearly 28% to over 45% higher than renting:

San Francisco-Oakland-Berkeley – 45.5%

Kahului-Wailuku-Lahaina, Hawaii – 44.5%

San Jose-Sunnyvale-Santa Clara, California– 41.3%

San Diego-Chula Vista-Carlsbad – 28.4%

Seattle-Tacoma-Bellevue – 27.9% (Tie)

Los Angeles-Long Beach-Anaheim – 27.9% (Tie)

Interested in the most undervalued housing markets in the U.S.? Stay tuned for the next article in this series featuring the U.S. News Housing Market Index.

Methodology

The U.S. News Housing Market Index is the most comprehensive collection of data points for the country’s largest metropolitan statistical areas that is also available for free on the internet. This data is sourced from a variety of government and private sources.

The overall index includes four subindexes:

The Demand HMI includes government data on employment, unemployment, household growth, building permits, consumer sentiment from the University of Michigan, median home sales prices from Redfin and observed, smoothed housing rental prices from Zillow.

The Supply HMI includes government data on housing supply, rental vacancy rates, construction costs, construction jobs, builder sentiment from the National Association of Home Builders and architectural billings from the American Institute of Architects.

The Financial HMI includes government data on interest rates and access to credit, delinquencies and foreclosures from Black Knight, and ratios of monthly mortgage and rental payments to local per capita incomes calculated by the index. Monthly mortgage payments assume conventional financing with 20% down at the average monthly 30-year fixed rate reported by Freddie Mac.

For the purpose of these rankings, per capita income for each MSA was estimated through May 2024 using a proprietary formula incorporating the most recent annual Census Bureau data for July 2022 (and reported in December 2023), monthly national personal income growth from the Bureau of Economic Analysis, and a calculation of each MSA’s relative per capita income growth versus the U.S. for 2020 through 2022.